Hong Kong Mortgage Application Document Checklist 2026 : Employees vs. Self-Employed – Quick Guide to 11 Steps

If you want to know what documents are needed for a mortgage application: banks require different documents depending on whether you're a salaried employee, self-employed, applying as a company, or buying a private or subsidized flat. The main types of documents include ID/passport, sale and purchase agreement, income proof, employment or business documents, and additional paperwork for special cases like government housing or refinancing.

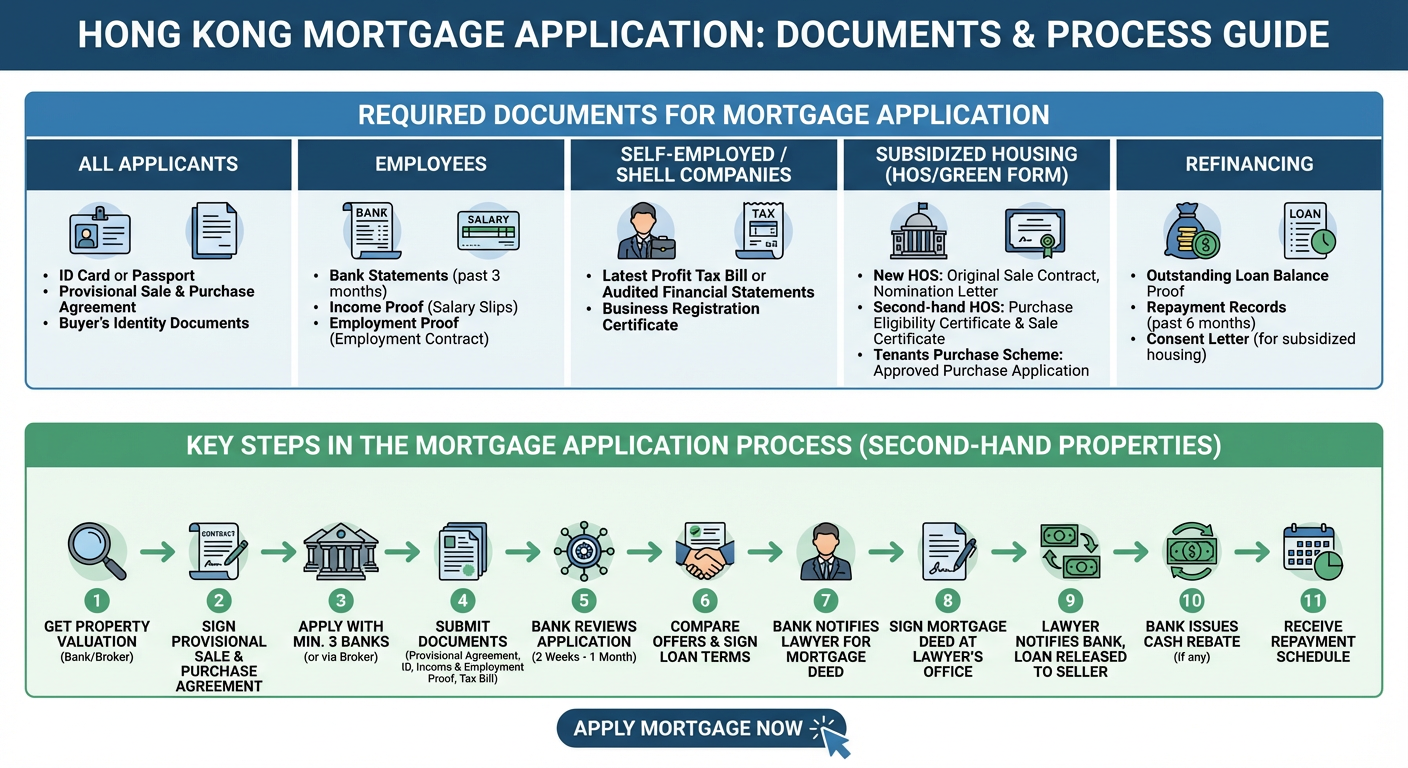

Required Documents for Mortgage Application

For all applicants:

- ID card or passport

- Provisional sale and purchase agreement

- Buyer’s identity documents

For employees:

- Bank statements from the past 3 months

- Income proof (salary slips)

- Employment proof (employment contract)

For government-subsidized housing:

The original Home Ownership Scheme (HOS) or Green Form Subsidised Home Ownership Scheme (GSH) Agreement and the respective Official Receipt for the deposit (for HOS/GSH)

- New HOS: Nomination Letter and Nomination Fee Receipt by Housing Authority

- Second-hand HOS: Certificate of Eligibility to Purchase by Housing Authority, Certificate of Eligibility for Sale from Seller

- Tenants Purchase Scheme:Letter of Offer issued and approved by Housing Authority

For self-employed:

- Latest profit tax bill or audited financial statements (including profit & loss and balance sheet)

- Business registration certificate

For shell companies:

Latest profit tax bill or audited financial statements (including profit & loss and balance sheet)

Business registration certificate

For refinancing:

Outstanding loan balance proof from current mortgage bank/financial institution

Repayment records from the past 6 months

Consent letter from the Housing Authority (for subsidized housing)

Key Steps in the Mortgage Application Process (for second-hand properties)

1. Get a property valuation from a mortgage broker or bank before signing the contract.

2. Sign the provisional sale and purchase agreement.

3. Apply for a mortgage with at least 3 banks, or use a broker for a one-stop application.

4. Submit documents: provisional agreement, ID copies, employment proof, at least 3 months of income proof (salary slips, bank statements, etc.), and latest tax bill.

5. Bank reviews your application (usually takes 2 weeks to 1 month).

6. Compare and choose the best offer, then sign the loan terms at the bank.

7. Bank notifies your lawyer to prepare the mortgage deed.

8. Before completion, buyer and guarantor (if any) sign the mortgage deed and other documents at the lawyer’s office.

9. Lawyer notifies the bank, which then releases the loan to the seller via the lawyer.

10. Bank issues any cash rebate for the mortgage.

11. Bank sends you a repayment schedule detailing principal, interest, and balance for each month.

;){kind=link}

;){kind=link}